Great experience since 1986

We have the necessary experience to organize and implement your business idea.

360° Services

We offer complete solutions, from the establishment of a company to its legal representation.

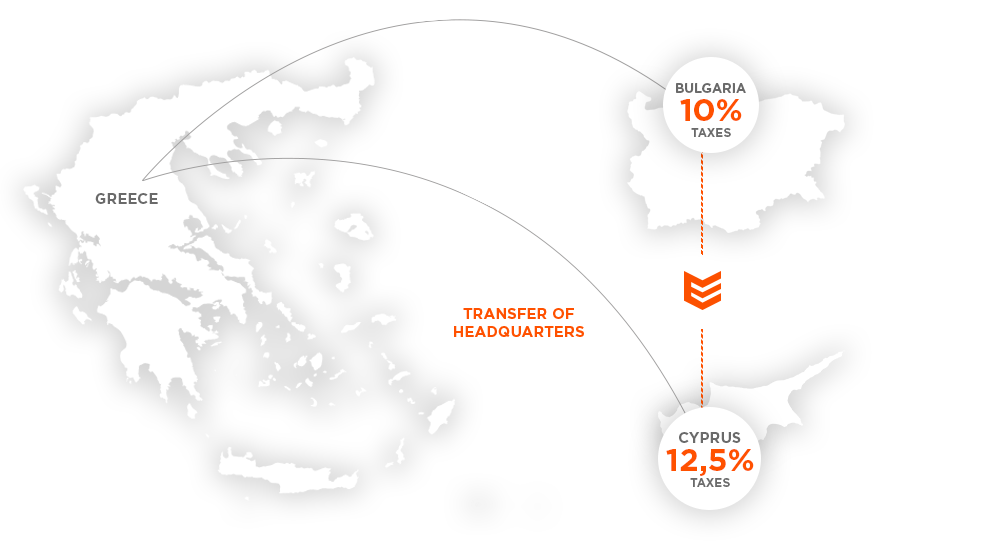

Personalised Tax Planning

We tailor our tax planning to your specific needs in order to achieve the right result.

High Specialization

Our considerable experience in setting up a company abroad is our passport to ensuring that your new venture is a complete success.